Last week, a tiny island of 23 million people quietly overtook the world’s fifth-largest economy in stock market value. Taiwan just surpassed India and the reason is a brutal wake-up call for every investor who still believes India’s market is unstoppable.

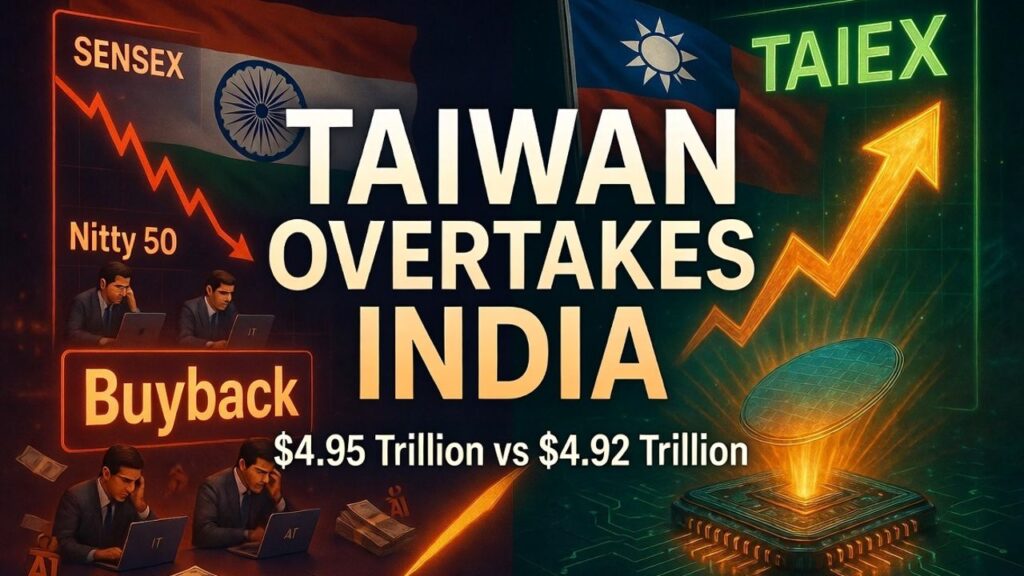

When Taiwan’s equity market cap edged past India’s last week $4.95 trillion versus $4.92 trillion it wasn’t just a statistical footnote. It was a stark, public verdict on two very different national strategies for building wealth in the AI era. Taiwan, a tiny island economy, now sits as the world’s fifth-largest stock market. India, the world’s fifth-largest economy, has slipped to sixth. The gap is razor-thin, but the message is loud: India’s market has been stuck in neutral since late 2024, delivering near-flat or negative returns while global peers powered by semiconductors and deep tech have surged.

The numbers tell the story clearly. The Sensex hovers around 76,000–76,500 points down roughly 7% over the past year and essentially unchanged in real terms since its 2023–early 2024 peak. Full-year 2025 delivered just 8.5% in rupee terms, the worst performance among major global markets. Meanwhile, Taiwan’s TAIEX has rocketed nearly 95% over the last 12 months, almost entirely on the back of TSMC’s 49% rally this year alone.

So why is India’s market “failing” to deliver the upside investors expected? The reasons are not cyclical bad luck. They are structural, self-inflicted, and interlinked.

1. Missed the Global AI Mega-Trend + High Starting Valuations

Taiwan’s overtake was hyper-concentration in semiconductors. TSMC alone accounts for 42–44% of Taiwan’s benchmark and over half the market’s total capitalization. The company’s dominance in advanced chips, built on decades of relentless R&D (8% of revenue) and massive CapEx, positioned it perfectly for the AI explosion.

India entered 2025 at elevated valuations after the strong 2020–2024 bull run. When earnings failed to keep pace, a classic “time correction” set in. India’s market is diversified into banking, IT services, FMCG, and consumer plays sectors with limited direct exposure to AI hardware. The very strength that built India’s IT outsourcing empire (predictable services revenue) has become a valuation ceiling. Global capital rotated toward “picks and shovels” plays in AI infrastructure.

2. Corporate Risk Aversion: Buybacks Over Breakthroughs

Most Indian tech giants remain wedded to a low-risk, high-payout model. Take Infosys as the poster child. In September 2025 it announced its largest-ever ₹18,000-crore buyback while its FY25 R&D spend was a mere ₹850 crore just 0.5–0.62% of revenue. The top five IT firms collectively returned nearly ₹4.8 lakh crore to shareholders between FY20 and FY25 (87% of net profits), choosing immediate EPS boosts over heavy investment in proprietary AI models, semiconductors, or deep-tech hardware.

Private-sector R&D intensity remains stuck at 0.23–0.4% of GDP. Taiwan spends 4% of GDP on R&D, the vast majority directed at electronics and semiconductors.

3. Investor Friction: Taxes and FII Exodus

Foreign institutional investors have pulled out a record ₹2+ lakh crore net in 2025–early 2026. The 2024 hike in Long-Term Capital Gains tax to 12.5% (no indexation) and the 2026 Securities Transaction Tax increases have made India less competitive versus zero-CGT hubs. Combined with high valuations and rupee weakness, the tax regime has accelerated capital flight.

Domestic retail investors have stepped in heroically SIP inflows remain robust at ₹25,000–32,000 crore monthly but they cannot fully offset the absence of patient foreign capital.

4. State-Level Populism: Freebies Crowding Out Future Growth

Even when the Centre launches ambitious programmes the ₹1 lakh crore RDI Fund, India Semiconductor Mission 2.0 execution lives with the states. The Economic Survey 2025-26 flags that unconditional freebies have exploded more than five-fold to an estimated ₹1.7 lakh crore this year. In several large states, committed expenditure now consumes 50–60% of revenue receipts, leaving little fiscal space for the land, power, water, and skilling infrastructure that semiconductor fabs and deep-tech clusters actually require.

The Silver Lining and the Urgency

India’s economic fundamentals remain strong: robust domestic consumption base, a young demographic, world-class digital public infrastructure, and a surging deep-tech startup ecosystem. The policy direction is also the most supportive it has ever been.

But the window is narrowing. If Indian corporates continue prioritising safe servicing revenue and buybacks, if taxes keep deterring long-term foreign money, and if too many states treat budgets as handout machines rather than growth engines, the Taiwan moment will not be a one-off warning it will become a permanent valuation gap.

The next 3–5 years will decide whether India builds its own deep-tech champions or remains a world-class applicator of other people’s technology. The market is watching. So far, it has voted with its feet.

The choice and the opportunity is still India’s to seize.