Every time you buy 10 grams of gold today, you are silently paying a ₹26,000 penalty for the weakening rupee.

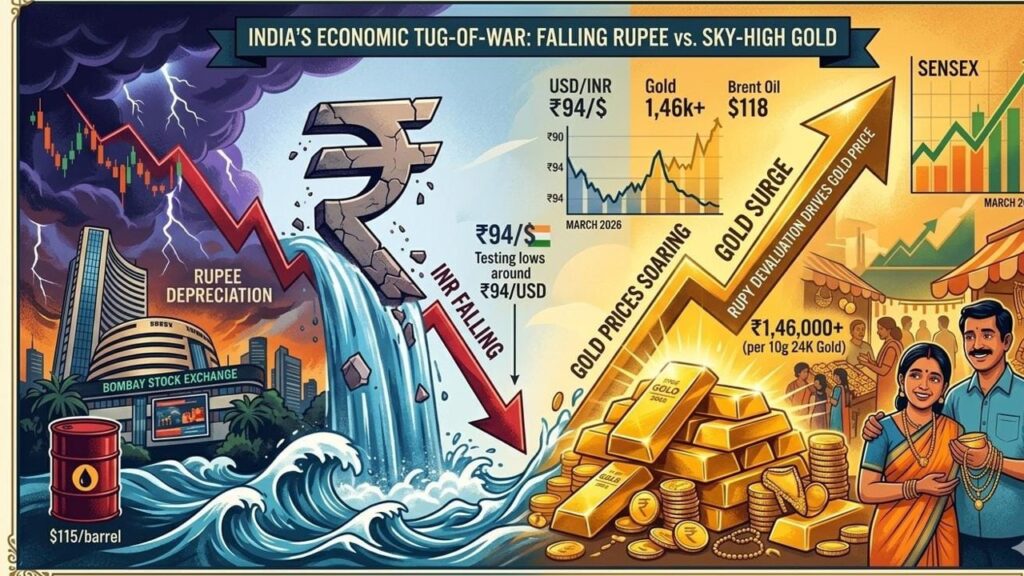

The Indian rupee has been sliding sharply in March 2026, repeatedly testing record lows around ₹94 per US dollar. For ordinary citizens tracking their expenses and savings, it often feels like an unrelenting “Niagara Falls” drop. This depreciation is not just a headline it is directly responsible for pushing gold prices in India to painful highs near ₹1,46,000–1,47,000 per 10 grams for 24K purity.

After nearly 12 years of the current government, many wonder why the rupee cannot be stabilised. The honest answer: Short-term firefighting by the RBI helps prevent a crash, but lasting stability demands faster structural reforms exactly the long-term plan India needs to reduce import dependence and build export muscle.

What’s Driving the Rupee’s Fall Right Now? The immediate trigger is the US-Israel-Iran conflict that escalated in late February 2026. Global oil prices spiked (Brent crude touching $100–120+ per barrel), forcing India which imports 88.6% of its crude oil (April–January FY26) to spend far more dollars. Foreign investors pulled out billions in a global risk-off mood a stark reminder of the dangers of relying on volatile “hot money” (Foreign Portfolio Investment) in the stock market rather than sticky, long-term Foreign Direct Investment (FDI) in manufacturing. Meanwhile, the US dollar strengthened as a safe haven.

The Reserve Bank of India (RBI) has responded by selling over $20 billion from forex reserves and managing liquidity through bond operations. These steps slow the fall and prevent disorderly volatility. However, as many have pointed out, repeatedly selling dollars and tweaking bonds offers only temporary relief. India follows a managed float system, meaning the rupee must respond to market realities. Artificially holding it risks exhausting reserves without solving root causes.

The Deeper Structural Challenge – And the Long-Term Roadmap India’s vulnerability comes from a chronic imbalance: heavy imports of oil, electronics, and gold versus slower growth in high-value manufactured exports. Frankly, if not for the massive dollar inflows from our booming IT services, Global Capability Centres (GCCs), and robust NRI remittances acting as a “Services Shield,” the current account deficit would be unmanageable, and the rupee might have already breached the ₹100 mark. This structural pressure has persisted for decades across governments, but external shocks amplify it.

The current administration has laid a clear foundation through Atmanirbhar Bharat, Make in India, and the Production Linked Incentive (PLI) schemes. Latest data (as of December 2025) shows PLI has:

- Attracted investments exceeding ₹2.16 lakh crore.

- Generated cumulative production/sales over ₹20.41 lakh crore.

- Created more than 14.39 lakh direct and indirect jobs.

- Driven exports from these sectors past ₹8.3 lakh crore.

Yet, the pace must accelerate. As discussed, short-term interventions alone won’t suffice. India urgently needs quicker action on:

- Reducing overall imports through deeper localisation in electronics, components, and critical materials. Initiatives like the India Semiconductor Mission (ISM) are absolutely vital here, as domestic chip fabrication is the only way to permanently slash the electronics import bill. Similarly, the ongoing push for defence indigenisation and rising defence exports serves as a prime model for plugging historical leaks in our dollar reserves.

- Rapid development of export-based manufacturing scaling PLI further, improving logistics, and signing effective free trade agreements (FTAs) so India earns more dollars instead of spending them.

- Tackling oil dependency head-on currently at nearly 89%. While domestic production remains stagnant, the government has diversified sourcing to over 40 countries (including discounted Russian oil) and built strategic reserves.

Accelerating the Shift to Alternative Energy and EVs Oil remains the single largest drain on the rupee during global price spikes. The good news is progress in renewables and EVs:

- Renewable energy capacity (excluding large hydro) stands at 266.68 GW as of February 2026, with solar crossing 143 GW. India achieved a 50%+ non-fossil share in power capacity five years ahead of target.

- Ethanol blending has reached 20%, and green hydrogen initiatives are gaining traction.

- On Electric Vehicles (EVs), sales touched 2.3 million units in 2025, with overall penetration rising to around 8% of new vehicle registrations. While adoption is stronger in two- and three-wheelers (at 5–6% and higher in some three-wheeler segments), it remains at only ~4% in passenger cars. Schemes like PM E-DRIVE and PLI for auto components are supporting this shift.

However, penetration is still low due to high battery import content (often from China), inadequate charging infrastructure, and higher upfront costs for buyers. Encouraging wider adoption of alternative energy sources requires bolder, faster measures: stronger incentives for local battery manufacturing, massive scaling of public charging networks, stricter domestic value-addition norms, and public awareness campaigns to change consumer behaviour. Bringing oil import dependence below 70% in the next decade would dramatically ease pressure on the rupee.

How Rupee Devaluation is the Major Driver Behind Sky-High Gold Prices Gold perfectly illustrates the rupee’s impact. Priced globally in US dollars, nearly all gold in India is imported. When the rupee weakens:

- The same quantity of gold simply costs more in Indian rupees.

- Safe-haven demand during uncertainty adds further upward pressure.

A striking example: If the rupee had remained stable in the ₹60–70 range (levels seen in the mid-2010s), today’s gold price in India would likely hover around ₹1,20,000 per 10 grams not the current ₹1,46,000+ levels. That extra ₹26,000+ per 10 grams is largely the hidden “rupee depreciation tax.”

During rupee weakness, many Indians also turn to gold as a traditional hedge against currency loss and inflation. This surge in domestic buying further inflates prices, making jewellery for weddings, gifts, or long-term savings far less affordable for middle-class families. Furthermore, these sky-high prices, compounded by import duties, historically incentivise parallel markets and smuggling. This creates a secondary headache for the government, forcing a tightrope walk between managing import duties to curb illegal inflows and trying not to drain forex reserves.

Real Impact on Normal People’s Lives A falling rupee quietly erodes purchasing power for millions:

- Fuel and daily expenses: Higher petrol, diesel, and LPG prices push up transport costs, cab fares, freight, and grocery bills.

- Inflation ripple: Each ₹1 depreciation can add roughly 0.2–0.3% to overall inflation, stretching household budgets.

- Big-ticket items: Smartphones, laptops, cars, fertilisers, and even some medicines become noticeably costlier.

- Aspirational costs: Overseas education, medical treatment abroad, or international holidays now demand 30–40% more rupees than a decade ago.

- Indirect burdens: Companies with dollar-denominated debt face higher repayment costs, which can eventually translate into higher prices or slower wage growth.

On the brighter side, exporters, IT/service professionals, and families receiving NRI remittances benefit as they receive more rupees per dollar earned. Still, for the vast majority of households, the short-term pain outweighs these gains.

The Way Forward: Faster Execution of Long-Term Reforms India does not need unsustainable artificial fixes that drain precious reserves. What it needs is accelerated implementation of the existing blueprint:

- Deeper localisation to cut import bills in electronics, EVs, and solar components.

- Speedier scaling of export-oriented manufacturing through PLI expansion and infrastructure upgrades.

- Aggressive promotion of EVs and renewables with practical incentives, better charging networks, and policies that make alternative energy accessible and attractive to ordinary citizens.

- Strategic geopolitical hedging through Rupee internationalisation. Expanding Special Rupee Vostro Accounts (SRVAs) and settling trade in local currencies with key partners bypasses the dollar entirely, offering a long-term shield against US currency hegemony and sanctions-driven oil shocks.

In conclusion, the rupee’s recent fall and its powerful role in driving up gold prices highlight an important economic reality. While the government has built strong foundations through Atmanirbhar initiatives, PLI schemes, and the renewable/EV push, the crisis reminds us that long-term vision must be matched by faster on-ground execution especially in reducing oil dependence and boosting manufactured exports.

For families planning big purchases like gold, careful timing and diversification matter. Ultimately, a stronger, more self-reliant manufacturing and energy ecosystem will benefit every Indian.